Housing Becomes Fluid Part 2

Housing Becomes Fluid Part 2

How iBuying will transform how we buy and sell homes

Last time, I looked at Airbnb’s effect on consumers’ relationship with homes, specifically, the increased flexibility if house renting became more fluid. Now, let’s focus on the biggest transaction the majority of Americans will make during their lives— buying a home.

Historically, home buying has been fraught with pain. Usually, purchasing a house involves coordinating an array of activities, each carrying a unique set of risks. The buyer may need to coordinate the sale of the current home with a new purchase, arrange for mortgage financing (takes 45-60 days on average), hire out a home inspection/cost assessment of needed repairs, secure homeowners/title/mortgage insurance, get a home appraisal, establish title, and pay a slew of fees to brokers, attorneys, escrow agents, and the bank.

All that can be headache-inducing. Add in the emotional attachment to a home which, on average, represents 24-33% of a person’s net worth, and home buying is ripe for disruption.

Keith Rabois, VC investor and co-founder of Opendoor, uses a famous formula when evaluating startup investments.

When disrupting an industry, two surefire ways to increase the probability of success are removing transactional friction and improving the customer experience. Historically, the real estate industry has done a mediocre job focusing on the experience of the end user, be it a residential buyer or a commercial office tenant. Outsized attention is given to the financing side of a real estate transaction, with little creative problem-solving energy directed at the person purchasing and occupying the space.

Over the past decade, technology transformed the transaction process of many industries, cutting down on friction and making the life of a buyer easier. E-commerce changed how people shopped, impacting the purchase of groceries, clothes, beauty products, consumer staples, and even cars. Digital platforms like Spotify, Netflix, and Roku transformed content consumption, aggregating songs, movies, and TV shows into a single platform.

Until recently, real estate transactions were laggards with regard to digital transformation. In 2020, the pandemic provided the perfect opportunity for this to change as consumers suddenly were unable to tour homes in person. Additionally, housing needs tend to change when people are forced to spend all their time inside, and with interest rates at historic lows, quicker transactions were in vogue.

Zillow and Opendoor sit ready to pounce on this shift with their search platforms and iBuyer model (iBuying refers to companies that utilize technology to make immediate offers on a home).

By removing friction and improving the customer experience when buying and selling a home, these companies will decrease the risk of transacting, and enable increased liquidity in the housing market.

Housing Becomes Fluid Part 2

Zillow’s Moat

Zillow began as a home listing platform, giving consumers the ability to search for homes in their market of choice. They understood human vanity, installing a “Zestimate” that put a price estimate on every single home in the US. The price estimate was primarily based on various MLS (multi listing service) systems and macro economic data points, and had previously not been front facing to consumers. Zillow created a listing page for any home, on or off market, and drove site traffic from people’s curiosity about their own home’s price or their annoying neighbor’s. In Kevin Kwok’s post, Making Uncommon Knowledge Common, he outlines how the Zestimate leveraged SEO to aggregate demand as well as supply for home buying:

The Zestimate became the kernel that Zillow used to create a webpage for every house. Zillow used its data content loop to become dominant at SEO for real estate. Try searching for your house on Google. I bet the first result is Zillow. And if not, it’s certainly in the top 5. Nobody had yet indexed all the homes in the US and brought them online. While sites like Apartments.com had started to do so for rentals, it wasn’t until Zillow (and Trulia) that this was done for homes. There was fertile search real estate to grab and Zillow rushed out to claim it all using the Zestimate as its spearhead.

Today, Zillow is a ubiquitous tool for home search, parodied in a SNL skit coining the term “Zillow Porn”— a concept referring to fantasizing about purchasing a home you see on Zillow (not watching homes have sex).

This cultural relevance creates an opportunity to convert passive buyers into active ones. The Zestimate adds a layer of legitimacy, anchoring the customer to a specific price point as they browse. Historically, price discovery has led to 2X higher conversion rates in E-commerce, a meaningful number when applied to a purchase as large as a home. The more time a consumer spends on Zillow, the better they are at recognizing value. If they see a home priced below what they deem it’s worth, their willingness to buy it will be higher. Historically, it’s been rare to take someone passively engaged in the home-buying process and convert them to an active buyer, but Zillow helps enable that through its listing supply and price discovery.

Much like Spotify did for music and Amazon for goods, Zillow aggregated the supply of homes and created a platform for consumers to discover them.

While this took hold, Opendoor started transforming the actual transacting of homes.

Opendoor and Transactions

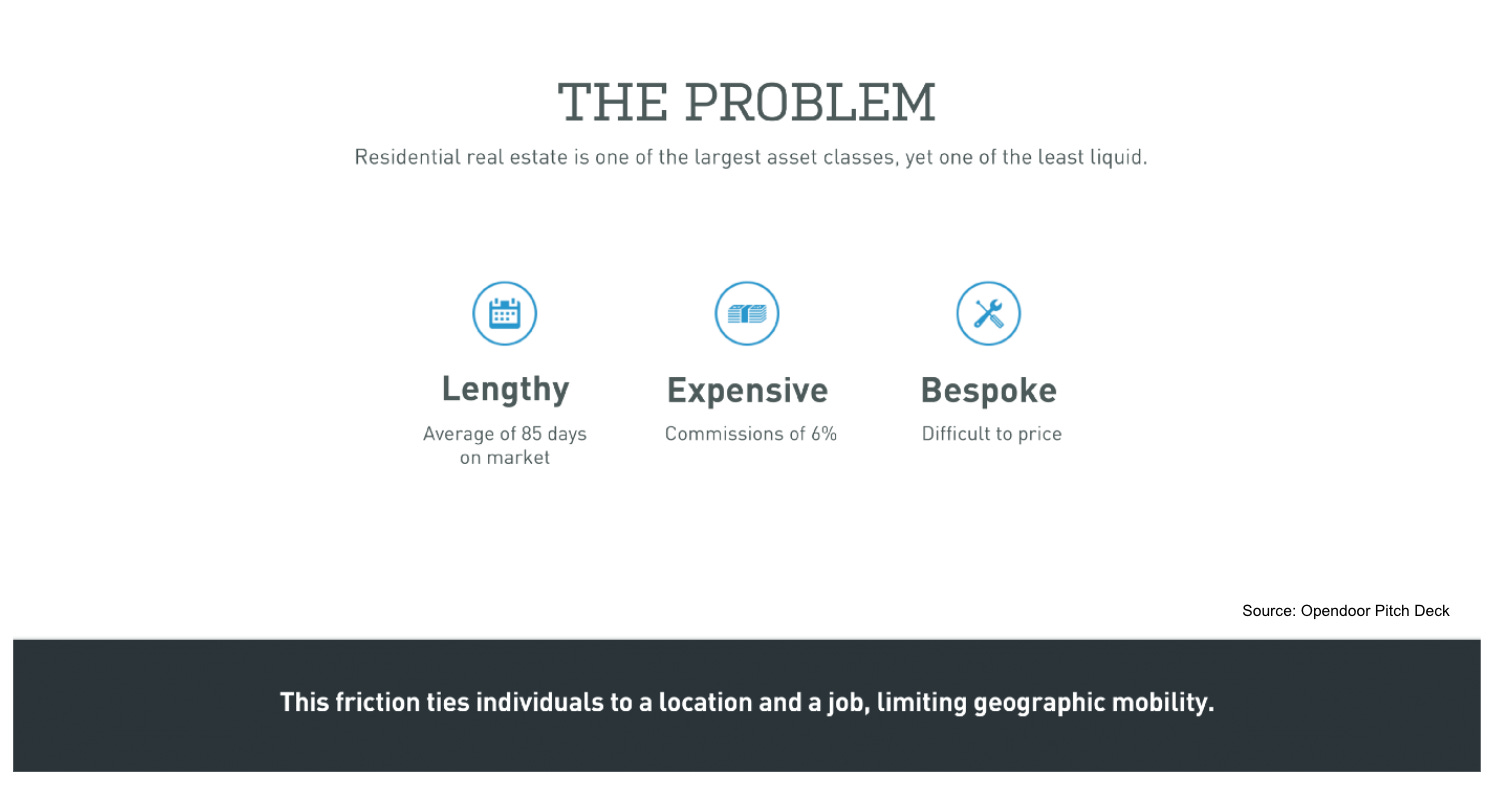

In its pitch deck for its Series A fundraise, Opendoor succinctly laid out the problem it aimed to solve.

The home-buying process is lengthy, expensive, illiquid, and filled with pricing errors. Due to this, individuals are tied to a location or job, which reduces their happiness as well as inhibits economic growth. The stats back this up. As of 2018, the median duration of homeownership in the U.S. is 13 years. Mobility rates are about half what they were in the 1940 and have been in a steady declining since the mid-1980s.1

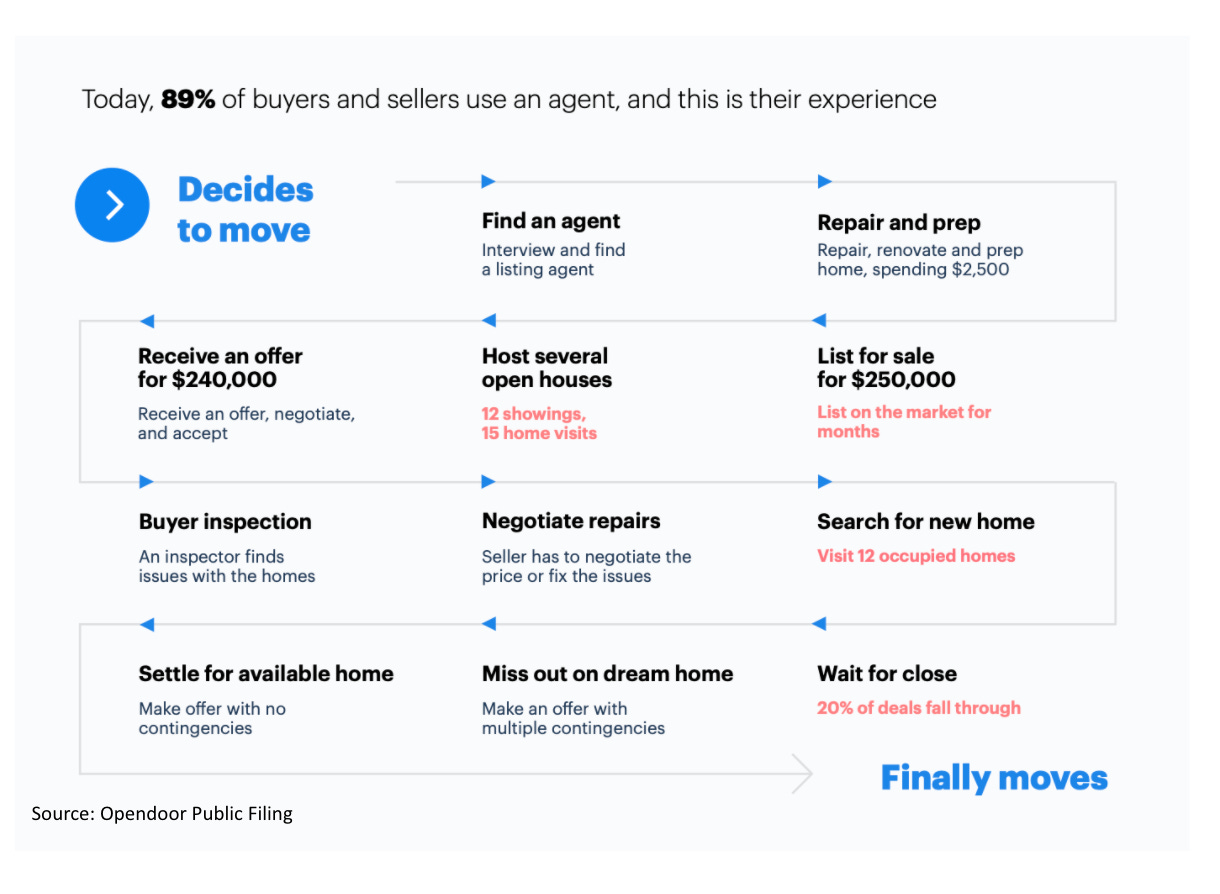

Flashing forward to 2020, Opendoor’s S4 public filing outlines the problem they solve in a similar fashion to their original pitch deck:

When Opendoor initially came to market, real estate experts met it skepticism. Many decried Opendoor as a glorified home flipper, and that interest rate fluctuations would be too difficult to manage. That makes sense if you’re analyzing the business purely from a real estate lens and discounting how new technology tends to change industries with historically low customer satisfaction.

On the podcast, Invest Like the Best, renowned Twitter account and anonymous hedge fund analyst, Modest Proposal, had this to say about the iBuying model:

“There have been three things in the last 15 years I said holy shit at. The first was Uber..the second was Airpods...and the third was iBuying. The minute I heard about it, I thought this is so obviously better than the existing way of selling your home...Traditional real estate people said at the time, “No you’re just a home flipper and what happens if prices go down”... Abstract a level above, ask yourself, are you solving a consumer problem here? Is this the most painful experience of a consumer’s life? Yes, it’s the largest transaction they do, but it's also probably the most painful. If you can provide a better way to do that, don’t you think you’re going to find some consumers want to. And if they do, don’t you think over time you can build an ecosystem around the 5.5 million existing home sales each year?”

People generally want things in their life to be easy, not hard. Once one gets a taste of that sweet frictionless transaction selling their home to an iBuyer, it’s doubtful they’ll want to return to the painful process outlined in the graphic above. In fact, they may feel more comfortable with the idea of moving in the future, knowing that Opendoor or Zillow can quickly snap of their home.

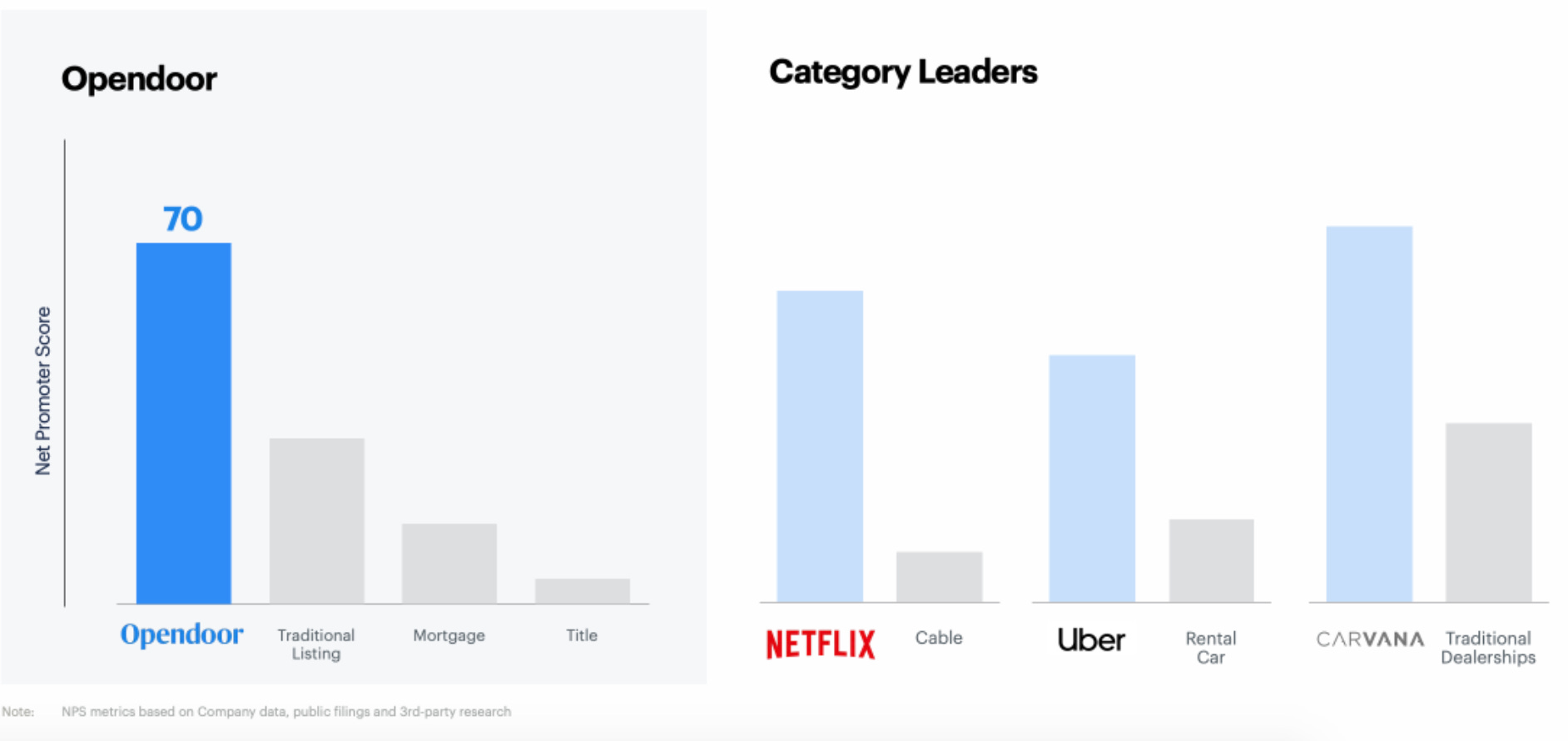

NPS (net promoter score) measures how likely a customer is to refer your service to a friend or colleague.

Opendoor rates highly compared to other residential housing services, resembling industry stalwarts such as Netflix, Uber, and Carvana. Carvana is an interesting example, as it faced similar industry skepticism when launching their online used car marketplace in 2012. Today, Carvana commands a valuation of $45B and achieved close to $6B in revenue for 2020.

On a different Invest Like the Best episode, Ram Parameswaran, founder of Octahedron Capital, explained why Carvana has excelled beyond competitors in the online used car space.

“It’s a delightful experience. You can pick the car, buy the car, and get financing in ten minutes or less. I’ve never seen a smoother transaction process of buying a car...It is the obsession on reducing friction that people just don’t get about Carvana, and none of their competitors come close to it.”

The easier a company makes it to transact with them, the higher the frequency of transactions. Sure, people don’t buy and sell homes at the rate that they purchase clothes or even cars, but decreasing the pain of housing transactions naturally enables sale velocity and frequency.

Bundling

Jim Barksdale, CEO of Netscape famously said: “There are two ways to make money in business: You can unbundle, or you can bundle.” A key factor for reducing the friction of housing transactions is the capability to bundle multiple services and streamline the process. In its S4 public filing, Opendoor highlighted several service areas it’s doing this, including:

Title and escrow: We offer customers seamless and integrated title insurance and escrow services through our affiliated companies. In the markets where our affiliates offer title insurance services, we provided title insurance services for 80% of Opendoor home transactions that closed during 2019, which helps validate our thesis that customers prefer an online, integrated experience.

Opendoor Home Loans: Launched in mid-2019, we have built this service from the ground up as a technology-first mortgage platform for customers looking to buy or refinance a home. We serve as a correspondent lender in the transaction and sell originated loans to third-party investors.

We are on the path to build a digital, one-stop shop that simplifies and streamlines the entire moving process. Today we offer title insurance, escrow and Opendoor Home Loans, with plans to add more services over time.

Becoming a true digital one-stop shop for the entire moving process is the holy grail. for iBuyers. As some of the more than 72 million millennials enter the housing market they will demand a digitally native and bundled offering for home transactions. A generation of people accustomed to trading stocks, paying taxes, buying clothes, and shopping for apartments online will demand an easier experience than the current home-buying process.

Additionally, creating a one-stop shop also gives Opendoor and Zillow pricing flexibility. According to Nima Wedlake, an investor in real estate startups with Thomvest Ventures, Opendoor’s ability to offer multiple services allows it to create bundling incentives.

For example, Opendoor may be willing to lower its home purchase fee (currently 6%-12%) if a customer agrees to finance their next home with Opendoor Home Loans, or purchases an Opendoor home insurance policy. Bundling may then improve seller conversion rates — according to Opendoor’s investor presentation, sellers are about twice as likely to sell their home at a 6% fee vs. a 12% fee.

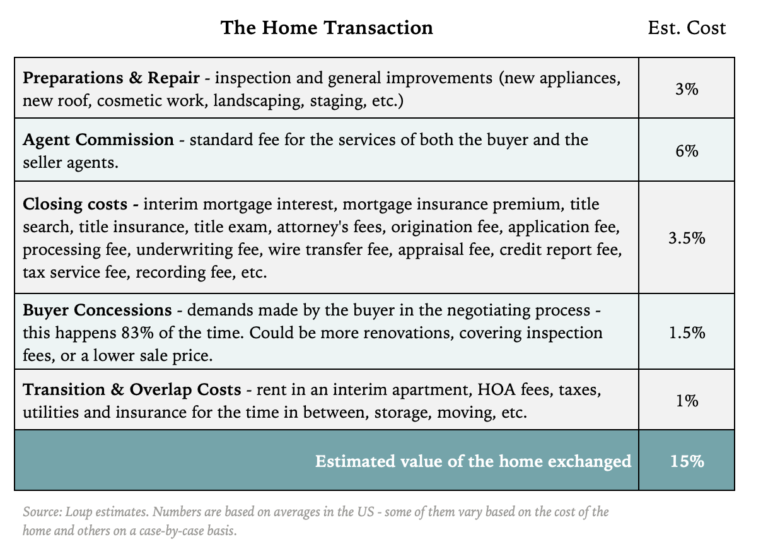

The more services iBuyers like Opendoor and Zillow bundle together, the more flexibility they have to offer incentives. Customers will likely be willing to pay a convenience fee to lower their purchasing risk, and Opendoor/Zillow can still decrease overall closing costs (currently around 15%!) for a consumer by cutting out third party intermediaries.

{kind=link}

Ultimately, Opendoor’s goal is to facilitate frictionless transactions for buyers and sellers on their platform. One of the easiest ways to do that is through the guaranteed financing of all cash offers, cutting out the length mortgage approval process.

According to Opendoor’s data, buyers who made offers with their cash-backed offer program have an average acceptance rate 50% higher than regular offers made without cash backing. All-cash home sales now make up about 36% of the market. Sellers find cash offers more attractive because there is less chance of the transaction falling through during the financing stage. This means you can present the certainty of an all-cash offer to the seller, free of financing, appraisal, and home sale contingencies, even if one need a home loan. And if you want to move into your next home before you sell your current one, Opendoor will even buy your new home for you.

The cash backed offer approach mirrors another nascent iBuyer, Ribbon, which originally came to market differentiating itself as a service providing all cash offers for buyers. Similarly, services like Knock and Orchard offered point solutions that enabled users to buy a home with cash before you sell yours through unlocking home equity up front or in a home swap.

Unfortunately for these startups, Opendoor and Zillow can easily integrate these add ons and customers want as much of a one stop shop as possible. Value is created through bundling the services together and cutting out steps in the home buying process for consumers.

Effect on Brokers

It’s clear that the rise of iBuyers makes the average consumer a winner. However, as is typical when industries change, there are parties that need to adjust.

Residential real estate brokers find themselves in a precarious position moving forward. The previously cumbersome transaction process confused customers and increased counterparty risk, necessitating broker involvement to build trust through expertise.

iBuyers’ ability to directly transact injects trust and speed into the process, vacuuming up value previously provided by brokers. It also sets a publicly visible price floor, hampering the negotiating leverage for brokers.

Additionally, virtual tours are beginning to disintermediate brokers giving house tours at the start of a search. If I’m looking to buy a house or rent an apartment, my first step is to go to Zillow or Streeteasy and look at my options. From there, I’ll browse the videos and photos to decide my best options before seeing any in person.

“The virtual home tour is here to stay,” said Redfin chief economist Daryl Fairweather in her housing market predictions for 2021. Consumer behavior towards virtual tours shifted during the pandemic, enhanced by companies like Matterport, a company that creates 3D tours of homes that recently went public via SPAC at a valuation of $2.9B.

Customer habit shifts tend to be sticky when it involves enabling convenience, and the majority of home searches going forward will begin online.

Brokers best option may be a Faustian bargain of working with the iBuying platforms for a lesser fee. Consumers will still see value in having a human shepherd them through the process, just not for 6% as the broker’s services become commoditized.

What’s Next?

As the growth of iBuying continues it will likely intersect with an increased frequency of remote work, covered in part one. As the home buying process improves, more people will be empowered to move. If one isn’t tied to a location through work, they may relocate to a new city if they have the security of a buyer in a matter of days. Enabling movement for those that want to live outside of the major job markets will be a benefit for our country and economy, decreasing wealth concentration from a handful of “superstar” cities.

Further, less transactional friction leads to higher liquidity for housing. Historically with stocks, higher liquidity meant lower volatility. More traders transacting at once typically results in less price fluctuations. As transactional volume increases and price discovery improves, we may see a reduction in housing market volatility over time.

Ultimately, the biggest winner of this shift will likely be Zillow. Recently, the company launched the Zestimate as the price for iBuying offers in select markets. This creates a flywheel effect around their sexiest feature, turning the Zestimate into a tool for demand aggregation as well as further price discovery. Zillow’s brand power serves as the ultimate demand barometer, turning clicks and views into a specific measurement of housing interest.

The inputs to the Zestimate include which homes see the most demand on its platform, strengthening its pricing power and aligning with what customers are truly willing to pay. The conversion rate of buyers and sellers within this ecosystem will be higher, as Zillow owns the top of the funnel. Quantifying and converting passive interest in real estate is difficult, and that’s what ultimately will set Zillow apart in a world of increased housing liquidity.

And for us consumers, we can keep dreaming about that mansion in North Carolina we want to buy.

Cheers,

Evan

https://www.jchs.harvard.edu/blog/who-is-moving-and-why-seven-questions-about-residential-mobility#:~:text=Mobility%20rates%20are%20about%20half,the%20past%20(Figure%202).